Office construction in Reno remained at low levels during Q1 2026.

Kidder Mathews recently released its Q1 2026 Reno Office Market Report. The amount of space under construction remained completely flat quarter-over-quarter at 215.1KSF. This demonstrates that the amount of space under construction was revised downward since the last report. (NVBEX; Jan. 15)

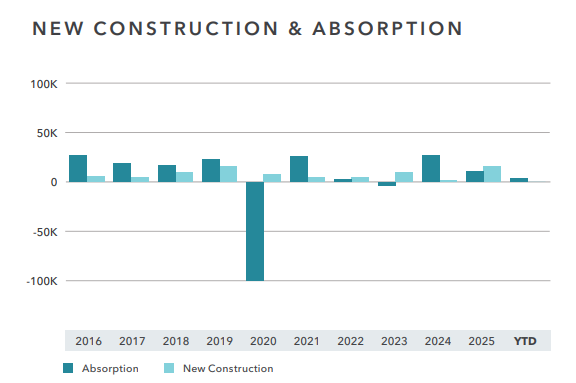

Q1 did not see a single construction start or delivery. The amount of space under construction has experienced a slight decline of 2.8%. Year-over-year, the amount of space actively under construction totaled 221.3KSF. Notably, Q4 2024, had 364.4KSF of office space under construction.

Vacancy rates showed a slight improvement and declined from 7.7% to 7.3% YoY. This reflects a total change of 40 basis points. In terms of QoQ data, vacancy rates fell from 7.5% to 7.3%.

Average asking rents experienced a slight increase at 1.5% YoY from $2.06/SF to $2.09/SF. This is still a decline QoQ, as Q4 2025 had an average asking rate of $2.13/SF.

The average sales price demonstrated behavior opposite to the average asking rents. It showed a QoQ increase and a YoY decline. Q1 2026 had an average sales price of $229.00/SF; Q4 2025 had an average sales price of $200.76/SF, and Q1 2025 had an average sales price of $259.85/SF. Percentagewise, the average sales price fell 11.9% YoY.

Cap rates ended Q1 at 6.5%. Both Q1 2025 and Q4 2025 had cap rates set at 6.3%. This reflects an increase of 20 bps.

Despite absorption being positive over the course of the quarter, it was still a steep decline. This quarter saw total net absorption at 35.7KSF. The previous quarter had an absorption of -38.7KSF. YoY, absorption fell by 32.3%, as Q1 2025 saw 52.7KSF absorbed.

To read the report in its entirety, click here.