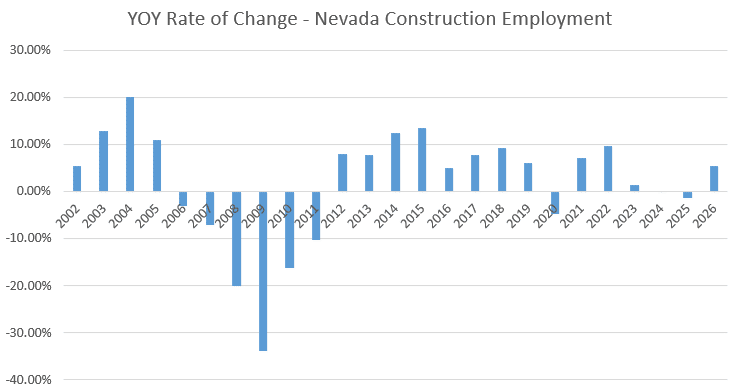

The Retail market in Reno has seen its contraction in overall construction activity continue into the year.

Kidder Mathews recently released its Q1 Reno Retail report. Highlights from the report include elevated vacancies, decreased unemployment, flat rental rates and a decrease in construction deliveries. NVBEX covered Kidder Mathews’ previous regional retail market report here.

Vacancy rates fell to 3.5% in Q1, which reflects an 80-basis point improvement year-over-year. Q1 2025 had a vacancy rate of 4.3%. Vacancies also experienced a quarterly improvement, with Q4 2025 having a 3.9% vacancy rate.

The average asking rent remained at $1.51/SF. This reflects an entirely flat continuation of Q4 2025. It has also remained flat in terms of year-over-year data, with an annual percent change of 0.22%.

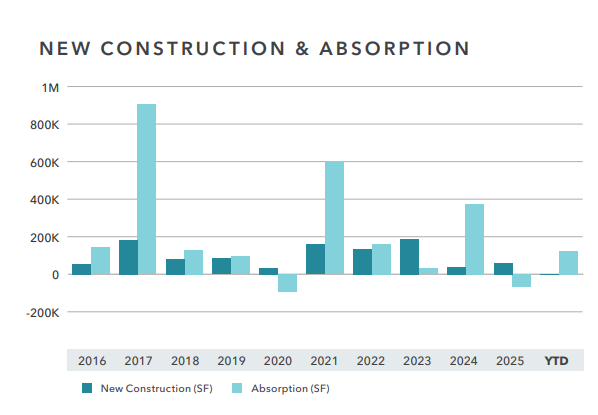

The amount of space under construction has continued to decrease, albeit more slowly. Quarter-over-quarter, the amount of space under construction fell from 102.5KSF to 100.8KSF. Q1 2025 had 133.9KSF of space, leading to a YoY decline of 24.69%.

The average cap rate saw both a QoQ and a YoY uptick of 0.6%, or 60 bps. Currently, the average cap rate sits at 6.6%, up from 6.0%.

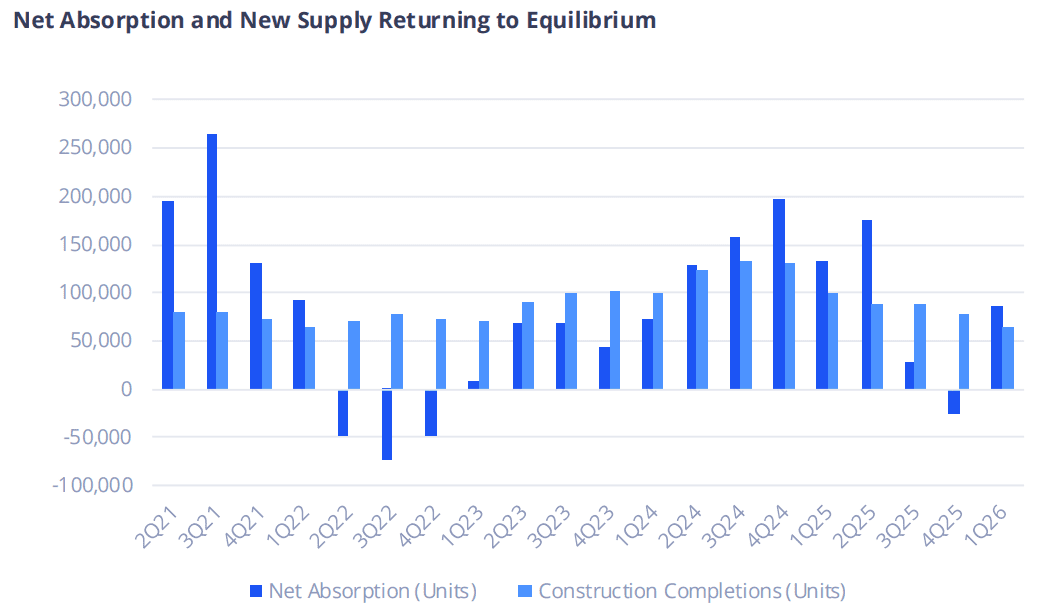

Deliveries in Q1 sat at 1.7KSF, which is a 91.39% decrease YoY. Q1 2025 had 19.3KSF in deliveries. Net absorption, however, experienced an increase from Q1 2025 to Q1 2026. Absorption finished the first quarter at 122.8KSF.

The average sales price saw a substantial increase QoQ from $231/SF to $299/SF. This is higher than the previous year, which was pegged at $272/SF, reflecting a 10.21% change. The full report is available here.